🚀 Medial Secures Investment on Shark Tank India - Fueling the Future of Professional Social Networking. 🔥

✕

Login

Home

News

Messages

Startup Showcase

Trackers

Premium

Premium Content

Jobs

Notifications

Settings

Try our Valuation Calculator →

Log In

News on Medial

Jobs platform Apna's revenue nearly triples, expenses rise in FY23

Inshorts

·

2y ago

Medial

Bengaluru-based job and professional networking platform Apna tripled its operating revenue in FY 2022-23, reaching Rs 180.3 crore. However, increased expenses resulted in higher losses compared to the previous fiscal year. The platform's total revenue, including interest income, reached Rs 188.1 crore. Expenses rose to Rs 308.4 crore, leading to losses of Rs 120.3 crore. Employee benefits accounted for the largest expense, amounting to Rs 203.8 crore. Apna reduced advertising and promotional expenses but still spent Rs 62.1 crore in this area. Apna became a unicorn in 2021 after raising $100 million in funding.

View Source

Related News

Gaming startup WinZO triples revenue

Inc42

·

1y ago

Medial

WinZO saw its consolidated operating revenue zoom nearly 3X to INR 673.94 Cr in the financial year ended March 31, 2023 (FY23). The Delhi NCR-based gaming major reported an operating revenue of INR 233.89 Cr in the previous fiscal year. In FY22, the startup reported a non-operating expense of INR 240.45 Cr.

View Source

Kuku FM’s FY25 revenue nearly triples to Rs 242 crore; net loss rises 59% - The Economic Times

Economic Times

·

2m ago

Medial

Kuku FM, an audio and video content platform, reported a 175% increase in operating revenue to Rs 242 crore for FY25, despite a 59% rise in net loss to Rs 153 crore. Total expenses more than doubled to Rs 411 crore due to increased advertising and marketing spending. The company, with over 10 million paying subscribers, recently closed an $85 million funding round and is preparing for a potential IPO.

View Source

Leverage Edu’s FY23 Loss Widens 118% To INR 102.8 Cr, Sales Surge 3.3X

Inc42

·

2y ago

Medial

Study abroad platform, Leverage Edu, experienced a significant rise in expenses, causing its loss to widen by 118% in FY23. The startup's operating revenue, however, saw a 3.3x increase, reaching INR 68.9 Cr. Leverage Edu's strategic focus for 2022 was on long-term investments, including improving content, community, and acquisition products. The company also reported substantial brand growth and increased investments in marketing and team expansion. Its total expenses rose by 153% to INR 173.5 Cr, primarily driven by other expenses and advertising costs.

View Source

Battery Smart’s revenue triples in FY24 but losses widen over 2X

Entrackr

·

10m ago

Medial

Battery Smart, a battery-swapping network for electric two- and three-wheelers, recorded a three-fold increase in revenue for the fiscal year ending March 2024. However, its losses also doubled as the Gurugram-based company aggressively pursued scale. Battery Smart’s operating revenue soared 193% to Rs 164 crore in FY24 from Rs 56 crore in FY23, as per its consolidated financial statements sourced from the Registrar of Companies (RoC). The company made additional Rs 23 crore from interest on financial assets which pushed its total income to Rs 187 crore in FY24. On the expense side, depreciation charges ballooned 3.8X to Rs 85 crore, while finance costs rose nearly 3.75x to Rs 45 crore. Employee benefit expenses increased 95.2% to Rs 41 crore. Interestingly, advertising expenses fell by 60% to Rs 8 crore during the said fiscal year. Overall, Battery Smart’s total expenditure more than doubled to Rs 327 crore in FY24 from Rs 125 crore in FY23. Despite strong top-line growth, Battery Smart’s losses widened significantly. The company posted a net loss of Rs 140 crore in FY24, more than double the Rs 61 crore loss in FY23. Its Return on Capital Employed (ROCE) and EBITDA margin stood at -18.34% and -5.35%, respectively. On a unit basis, the company spent Rs 1.99 to earn a rupee in operating revenue. As of March 2024, the Gurugram-based firm reported current assets worth Rs 328 crore including Rs 107 crore in cash and bank balance. According to startup data intelligence platform TheKredible, Battery Smart has raised a total of approx $192 million of funding till date, having Tiger Global and Blume Ventures as its lead investors. Its co-founders Pulkit Khurana and Siddhart Sikka together own 28.5% of the company. Battery Smart remains one of the better positioned firms to benefit from the increased electrification of mobility in India, particularly two and three wheelers. The firm has incurred high costs as it establishes the best SOP and learns, never an easy task in a complex market like India. What probably helps it is the almost complete focus on B2B segments. The biggest risk factor of course remains the pushback from large manufacturers to have proprietary batteries, or a preference to build their own swapping networks as seen in the case of Honda recently. However, Battery Smart continues to have a lot going for it particularly in the three wheeler segment, where the swapping model trumps charging for now, by saving time and ensuring higher usage of the vehicle.

View Source

Kuku FM nearly triples FY25 revenue to Rs 242 crore; loss widens to Rs 153 crore

IndianStartupNews

·

2m ago

Medial

Kuku FM experienced significant growth in FY25, nearly tripling its operating revenue to Rs 242 crore from Rs 88 crore the previous year, driven by increased advertising expenses. Despite the revenue surge, the company’s net loss widened by 59% to Rs 153 crore due to aggressive marketing spending. Founded in 2018, Kuku FM offers long-form audio content and has about 10 million paying subscribers. The company is planning an IPO to raise up to Rs 3,000 crore.

View Source

Rapido’s FY23 loss widens over 50% to INR 674.5 Cr, sales jump 3X

Startup News FYI

·

2y ago

Medial

Ride-hailing startup Rapido reported a widened standalone loss of INR 674.5 Cr in FY23, a 53.6% increase from the previous fiscal year. The increased loss was primarily due to a sharp jump in employee costs and despite a significant rise in operating revenue. The company's total expenditure also increased by 96.3%, with employee expenses accounting for 17% and advertising expenses contributing 20.5% of the total expenses. Rapido, which provides auto and bike taxi services, raised $180 Mn in funding in FY23 and expanded its operations into cab services.

View Source

Healthkart’s revenue nears Rs 1,400 Cr in FY25; profit triples

Entrackr

·

4m ago

Medial

Healthkart’s revenue nears Rs 1,400 Cr in FY25; profit triples HealthKart, a nutrition and supplement e-commerce platform, recorded a 3X year-on-year jump in profit after turning profitable in FY24. The Gurugram-based company’s sharp profit growth was steered by strong sales momentum and a controlled cost structure. Healthkart’s operating revenue grew 29% to Rs 1,313 crore in FY25 from Rs 1,021 crore in FY24, according to its consolidated financial statement sourced from the Registrar of Companies (RoC). HealthKart owns and manufactures eight nutritional brands including popular supplement brands like MuscleBlaze, The Protein Zone, TrueBasics, HKVitals, bGreen, Nouriza, and Gritzo. Sales of products formed 97% of total revenue which rose by 29% to Rs 1,277 crore in FY25. Collections from services also increased by 16% to Rs 36 crore. Notably, non-operating revenue increased to Rs 55 crore in the last fiscal year from Rs 48 crore in FY24. The cost of materials accounted for the largest share of the company’s expenditure at 49%. To the tune of scale, this cost rose 26% to Rs 623 crore in FY25 from Rs 495 crore in FY25. Advertising spend saw a sharper rise of 39% to Rs 263 crore, while commission expenses increased 22% to Rs 82 crore. In contrast, employee benefit costs declined 5% to Rs 115 crore. Overall, Healthkart managed to keep its cost growth below revenue expansion. Its total expenses rose 23% to Rs 1,273 crore in FY25 from Rs 1,032 crore in FY24. The company’s profit surged over 3X to Rs 120 crore in FY25, while its ROCE and EBITDA margin improved to 5.45% and 6.02%, respectively. On a unit basis, Healthkart spent Re 0.97 to earn a rupee of operating revenue in FY25, compared to Rs 1.01 in FY24. As of FY25, its current assets stood at Rs 971 crore including Rs 73 crore in cash and bank balances. According to startup data intelligence platform TheKredible, Healthkart has raised a total of $382 million of funding till date, having Peak XV Partners, Temasek and Sofina as its lead investors. The company’s founder and CEO, Sameer Maheshwari owns 12% of the company.

View Source

Magicpin triples revenue to Rs 870 Cr in FY24, cuts losses

Entrackr

·

1y ago

Medial

Magicpin triples revenue to Rs 870 Cr in FY24, cuts losses Hyperlocal retail platform Magicpin demonstrated notable financial results, scaling nearly three-fold during the last fiscal year, which ended in March 2024. Moreover, the Gurugram-based firm managed to control its losses by 25% in the same period. Magicpin’s revenue from operations surged 2.92X year-on-year to Rs 870 crore in FY24 from Rs 297 crore in FY23, its annual financial statements sourced from the Registrar of Companies show. Magicpin, a hyperlocal retail platform, has partnered with over 500 brands and 20,000 fashion stores across India. The sale of vouchers contributed 92% of its total operating revenue, making it the primary revenue source for the Lightspeed-backed firm. Additional revenue came from commissions and ONDC subsidies. The company earned an additional Rs 9.6 crore from interest on deposits and investment gains, bringing its total income to Rs 880 crore in the last fiscal year from Rs 315 crore in FY23. Magicpin has launched MagicFleet, an AI-powered SaaS platform that onboarded over 40,000 riders in its first four months and now processes more than 3,00,000 orders per month. The company plans to expand this to 1,00,000 riders and 1 million deliveries. It introduced magicNow, a feature designed to meet the increasing demand for fast deliveries. For the reward platform firm, the procurement of vouchers was the largest cost center, forming 80.7% of the overall expenditure. To the tune of scale, this cost grew 3X to Rs 776 crore in FY24 from Rs 253 crore in FY23. The firm managed to keep its employee benefits flat and its advertising cost was reduced by 15% in the previous fiscal. Its delivery charges, technology, server, payment gateway, legal, and other overheads pushed the total expenditure to Rs 961 crore in FY24. The three-fold surge in scale coupled with controlled expenditure helped Magicpin to reduce its losses by 25% to Rs 78 crore in FY24. Its ROCE and EBITDA margins stood at -49.7% and -8.67%, respectively. Magicpin’s cost efficiency improved, with Rs 1.10 spent to earn a rupee in FY24. At the end of the last fiscal year, its total current assets stood at 196 crore with the cash and bank balance of Rs 50 crore. We excluded ESOP costs from the loss calculation as they are non-cash expenses. Magicpin reported that FY 2024 was a transformative year, establishing itself as India’s largest hyperlocal startup, the third-largest food delivery app, and the largest seller app on ONDC for delivery, according to CFO Chunky Shah. Magicpin has grown without raising external funds in the past two fiscal years. In November 2021, it secured $60 million in a Series D round, with Zomato investing $50 million for a 16% stake. According to TheKredible, Lightspeed is the largest stakeholder, holding a 34% stake in the firm. Launched well after the first startup rush into ecomm but early enough to avoid some of the worst excesses, Magicpin has done well to outlast many of its peers since it started in 2015. Leaving it well placed to take advantage in a market that has evolved considerably, and no longer demands the kind of burn rates we saw till about 2020. As a leader in the ONDC space, Magicpin has gained a strategic advantage and appears well-positioned to leverage new opportunities. The company, often seen as a quiet performer, may still have more surprises in store.

View Source

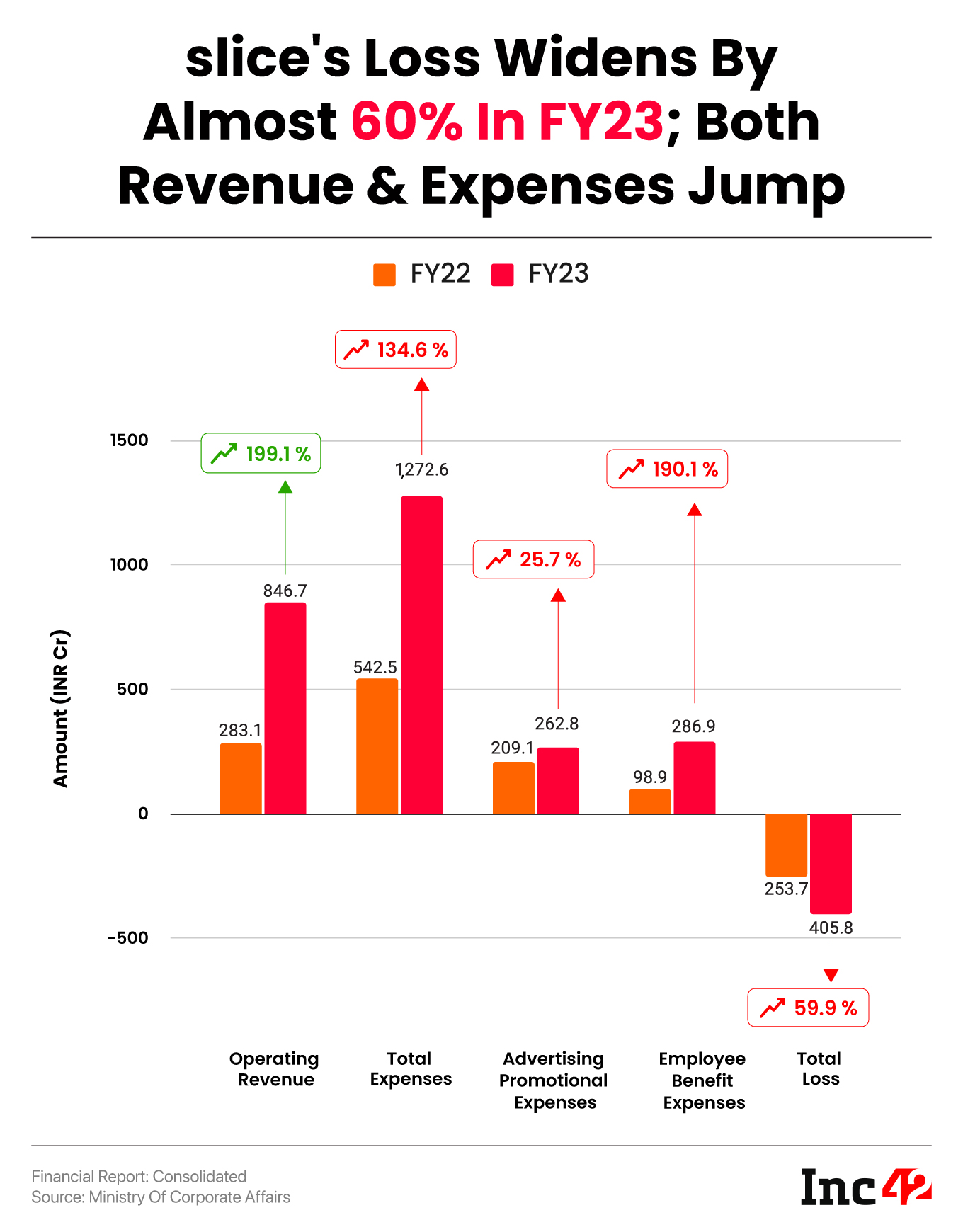

Fintech Unicorn slice spent INR 1.5 to earn every rupee in FY23

Inc42

·

2y ago

Medial

Garagepreneurs Internet Private Limited (GIPL), the parent company of fintech unicorn slice, saw a 60% increase in its consolidated net loss to INR 405.8 Cr in FY23. This loss was attributed to higher operating expenses and a decrease in assets under management. Despite a significant rise in operating revenue, slice's bottom line was affected by regulatory changes. The company shifted its focus to personal loans and UPI payment services after the Reserve Bank of India imposed restrictions on credit offerings. slice's total revenue in FY23 stood at INR 867.8 Cr, while total expenses more than doubled to INR 1,272.6 Cr.

View Source

Ferns N Petals posts Rs 607 Cr revenue in FY23; loses Rs. 110 Cr

Entrackr

·

2y ago

Medial

Ferns N Petals, a gifting platform, experienced a growth plateau in FY23 with only a 4.8% increase in income and heavy losses of nearly Rs 110 crore. Their revenue from operations reached Rs 607 crore in FY23, primarily from selling cakes, flowers, and customized gifting solutions. The company also operates in the hospitality and wedding businesses. The cost of procurement of materials accounted for the largest expenditure, while advertising and marketing, legal professional, freight, and IT expenses pushed the total expenditure up by 25%. As a result, Ferns N Petals posted a loss of Rs 109 crore in FY23, compared to a profit of Rs 10 crore in FY22.

View Source

Applied Jobs

Saved Jobs

Download the medial app to read full posts, comements and news.

Go to Medial App

Not Now

Know everything that’s happening in the startup ecosystem, first.

Enable Notifications?

No, thanks

Count me in

/indianstartupnews/media/agency_attachments/s1FnhAYONODoxNkoC8xA.png)